One KYC.

Every institution.

Zero re-submission.

Sovio Parichay turns a single verified KYC into a portable, consent-driven token - reusable across banks, fintech, insurance, telecom and travel. No repeated submissions. No data sprawl. RBI-aligned by design.

KYC is repeated everywhere - and that is the failure.

Manual identity verification slows onboarding and creates unnecessary operational friction.

Collecting and storing sensitive identity documents creates privacy, security, and compliance risks.

Reusable KYC engineered for every regulated institution.

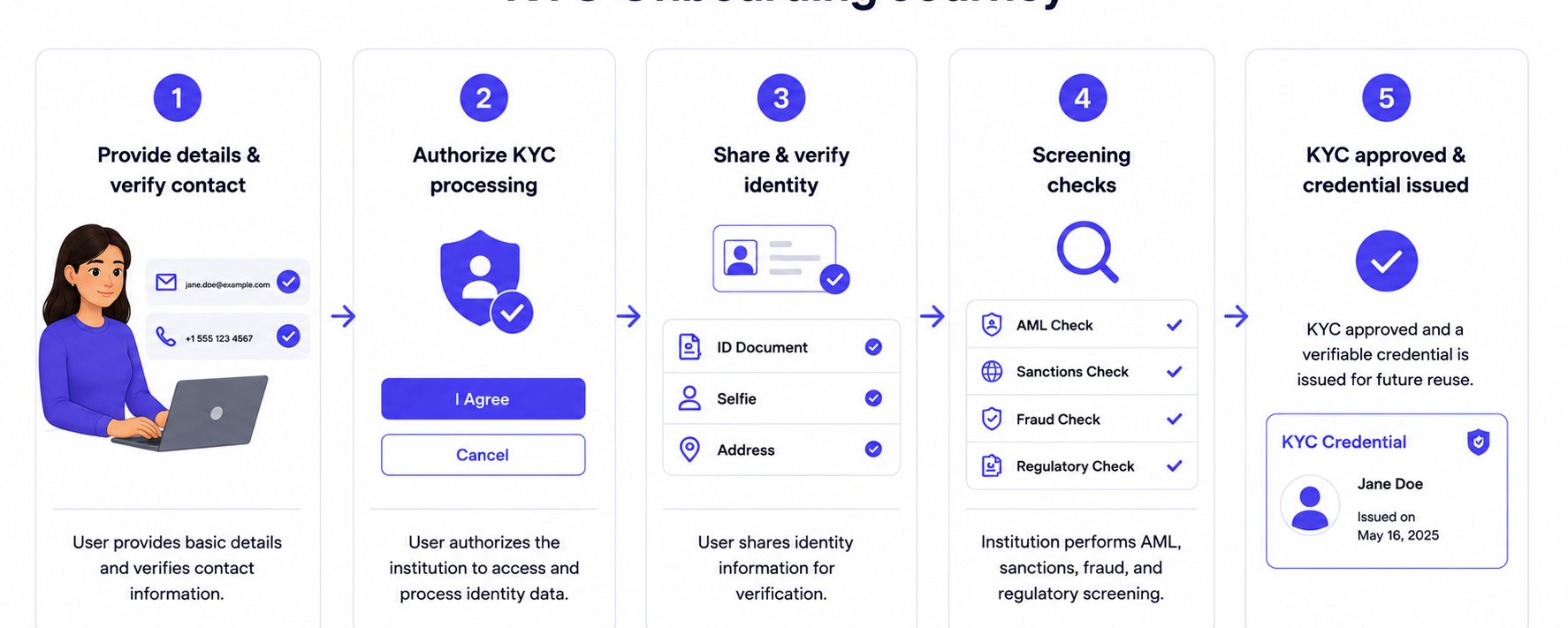

Complete KYC once at any regulated institution

User completes full KYC - Aadhaar, PAN, address proof - at a bank, fintech or KYC-ULA. Standard RBI process, executed once.

This is the only time the customer submits raw documents.

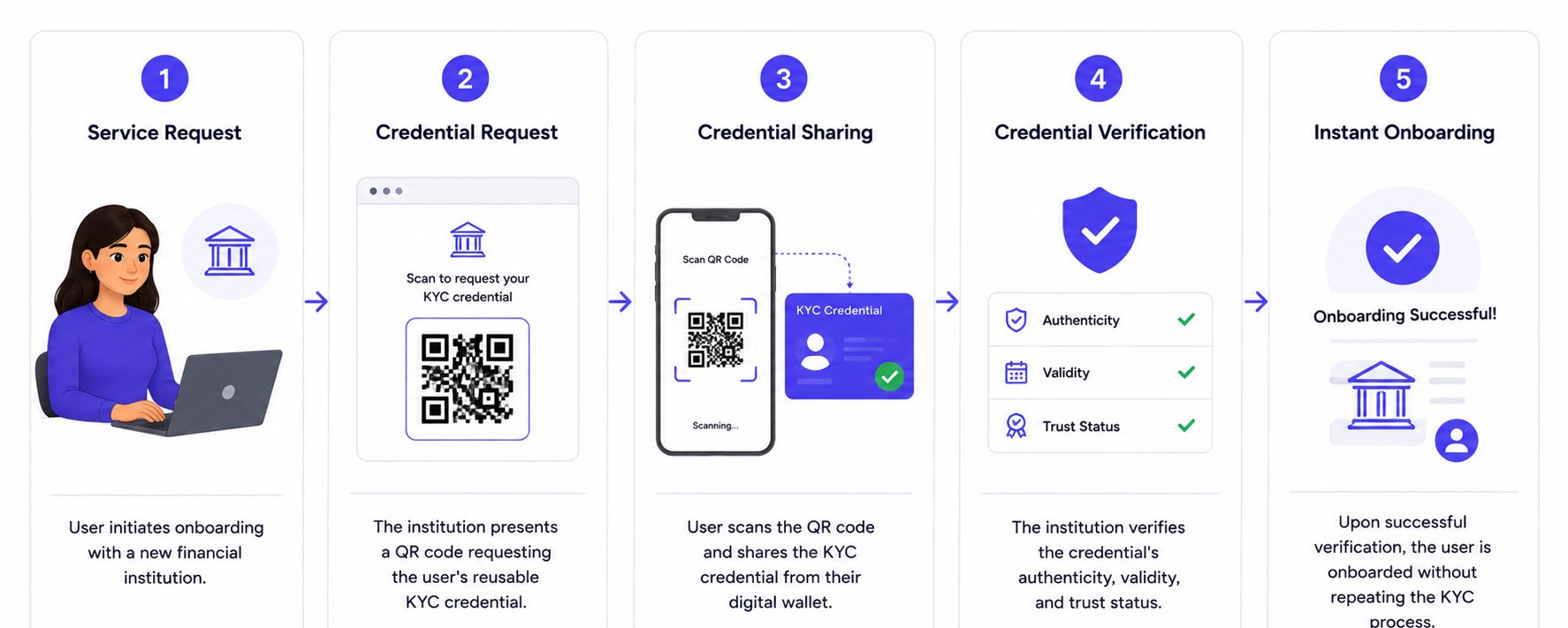

Reusable KYC — onboard in seconds, not days.

From token issuance to KYC verification — two workflows that eliminate redundant document submissions.

Six guarantees. Not policy - properties.

- 01Personal data never leaves the issuing institution.

- 02Tokens are cryptographically signed and tamper-evident.

- 03Every share is governed by a revocable consent receipt.

- 04Verification is offline-capable - no issuer round-trip.

- 05Tokens are revocable by user or issuer; time-bound by default.

- 06Compliance is built-in: RBI Master Direction, DPDP Act, IT Act.

Built on RBI directions and open identity standards.

Aligned with the directions, standards and consent architecture your compliance team already trusts - across banking, identity and data protection.

See Sovio Parichay

in your ecosystem.

Schedule a personalised demo to see tokenised reusable KYC running in your environment.